The thought of investing can be daunting to some. To help, we’ve compiled a series of questions every investor should ask themselves and be able to answer.

1. What age will you/did you start investing?

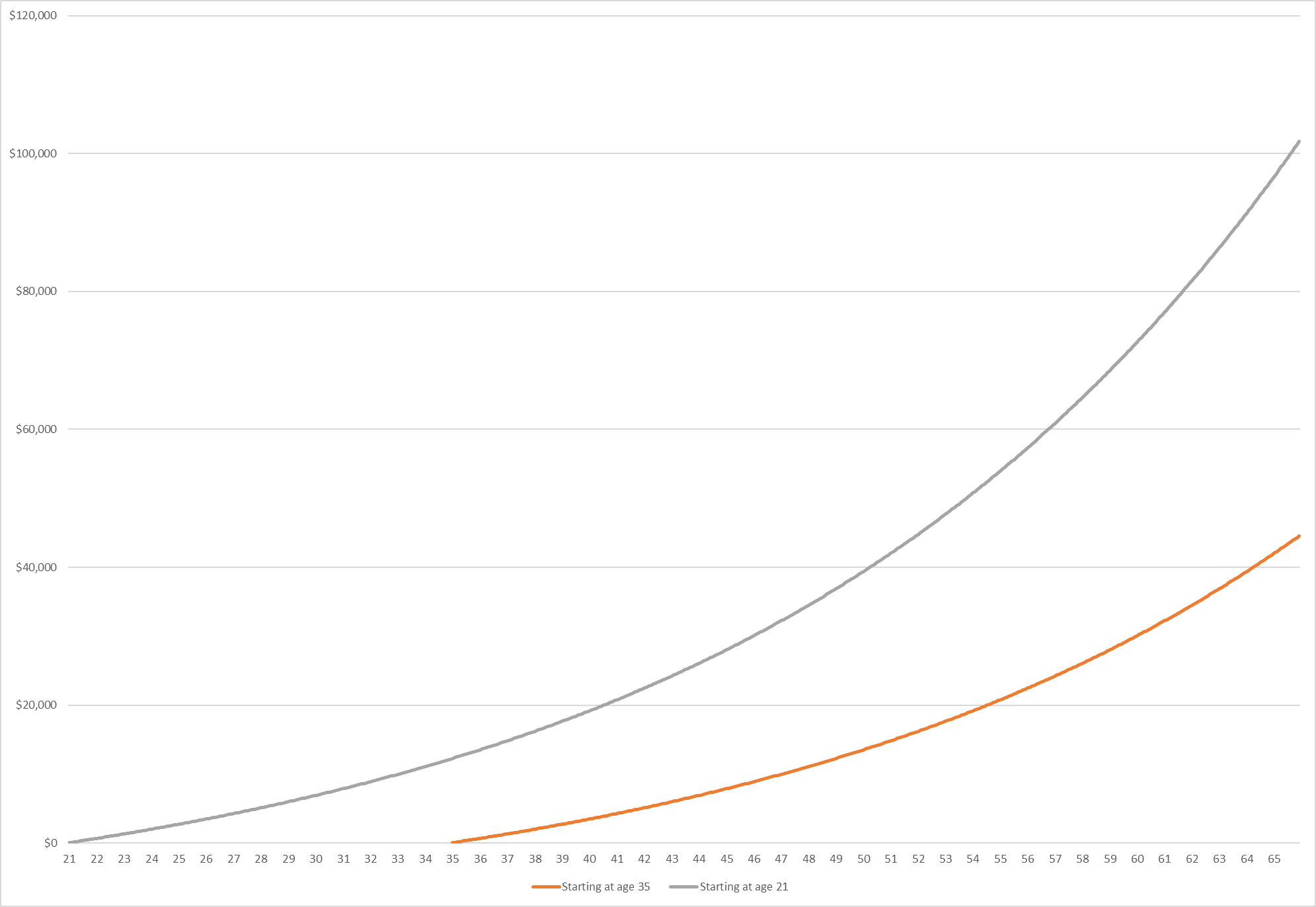

The earlier you start investing, the quicker your savings can grow.

Say, you’re 35 and you’re investing $50 a month over 30 years. Assuming your investments grow at 5% annually, you will have amassed savings of $44,541 by the time you are 65.

However, if you started investing at 21, your investment, based on the same logic as above, would be worth $101,744 by age 65. By starting earlier, your investment ends up being over 2.2 times larger (unadjusted for inflation).

2. Have you spread your money around?

Diversifying your investments means buying different types of investments, potentially across different countries and/or asset classes. Diversification doesn’t guarantee you won’t lose money but it can help to balance portfolio returns when a certain investment underperforms.

3. How much risk are you willing to take?

The risk spectrum, from low to high, generally moves from cash/savings; government bonds, corporate bonds, high-yield corporate bonds, developed market shares, to emerging market shares and alternatives. The higher on the spectrum, the greater the risk.

4. What is your time horizon?

Having a clear understanding of when you want to access your money could help you determine what type of investment is right for you. For instance, if you’re saving for a short-term goal, like a holiday, you may not want your money tied up in an investment which can fluctuate dramatically. For longer-term goals, you may be able to take on more risk as you have more time to allow for potential losses to be recouped.

5. Will you reinvest your income?

Investments typically generate income: shares pay dividends, bonds pay coupons, savings accounts pay interest. You can elect to receive this income as cash or you can reinvest this income to increase your investment.

If you elect to reinvest your income, this can trigger the effect of compounding. Compounding is earning interest on interest and it can help an investment grow at a faster rate.

Say you invested AU$1,000, 10 years ago and decided to take the income from this investment as cash. Your investment would currently be worth AU$1,501 (equivalent to an average annual return of 4.1%). However, if you had opted to reinvest the dividends, buying more shares, your current shareholding would be worth AU$2,310 (an average annual return of 8.7%).

So whether you are a seasoned investor or starting out on your journey, it’s important to ensure you ask yourself these important questions and speak to your financial adviser who can help you decide what’s right for you.

Remember, past performance is not a guide to future performance and may not be repeated. The value of investments and the income from them may go down as well as up and investors may not get back the amounts originally invested.

Important Information

Opinions, estimates and projections in this article constitute the current judgement of the author(s) as at the date of this article. They do not necessarily reflect the opinions of Schroder Investment Management Australia Limited, ABN 22 000 443 274, AFS Licence 226473 ("Schroders") or any member of the Schroders Group and are subject to change without notice. In preparing this article, we have relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources or which was otherwise reviewed by us. Schroders does not give any warranty as to the accuracy, reliability or completeness of information which is contained in this article. Except insofar as liability under any statute cannot be excluded, Schroders and its directors, employees, consultants or any company in the Schroders Group do not accept any liability (whether arising in contract, in tort or negligence or otherwise) for any error or omission in this article or for any resulting loss or damage (whether direct, indirect, consequential or otherwise) suffered by the recipient of this article or any other person. This article does not contain, and should not be relied on as containing any investment, accounting, legal or tax advice. Before making any decision relating to a Schroders fund, you should obtain and read a copy of the relevant disclosure document for that fund to consider the appropriateness of the fund to your objectives, financial situation and needs. You should note that past performance is not a reliable indicator of future performance. Schroders may record and monitor telephone calls for security, training and compliance purposes.

Source: Schroders